M&A is turning Japanese

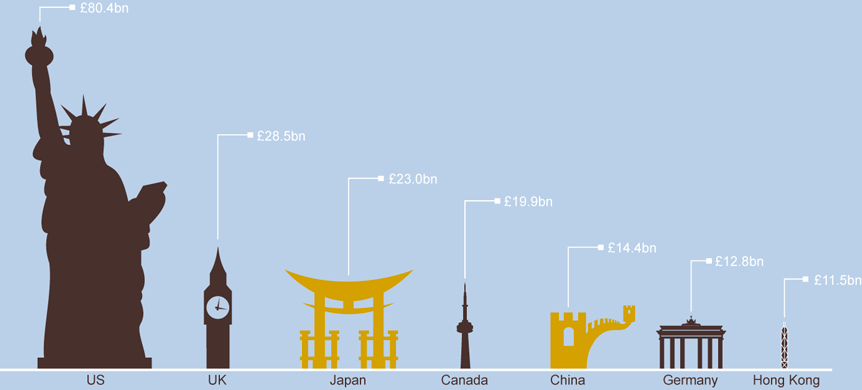

The world's most acquisitive countries*

In 2011 Japan became the world’s third most acquisitive nation; Asian investors have continued to buy assets abroad throughout 2012, with a particular focus on Europe.

|

US | £80.4bn |

|

UK | £28.5bn |

|

Japan | £23.0bn |

|

Canada | £19.9bn |

|

China | £14.4bn |

|

Germany | £12.8bn |

|

Hong Kong | £11.5bn |

*Value for the LTM (Last twelve months to end of October 2012). Mid-market transactions only i.e. transactions defined as £50m - £1bn. Outbound M&A

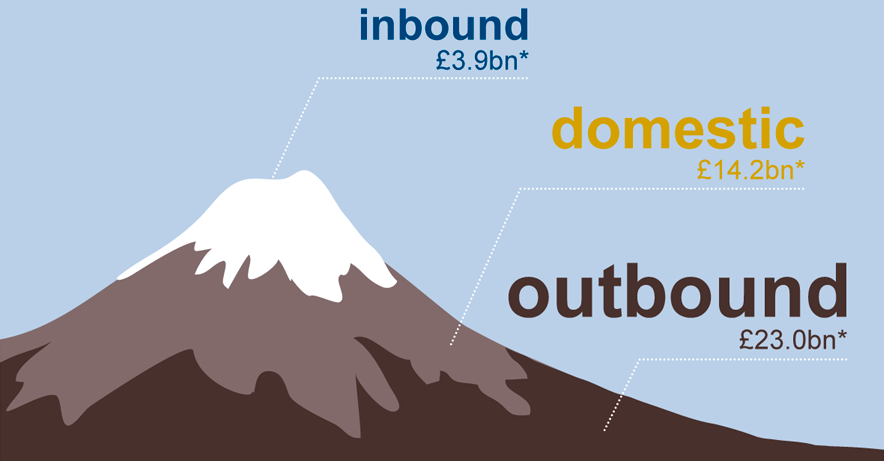

Japan overseas acquisitions 95-2012

Japan M&A

Japan a global investor

M&A was once regarded as cheating in Japan but weary of relentless decline in their home market and the effect of the strong yen eroding export margins, a new generation of Japanese management is emerging. As a result, Japanese companies have developed into global investors searching for acquisition opportunities abroad.

The tragic tsunami in 2011 crystallised attitudes. Japan had adapted in order to contend with low cost competition from China by developing some of the most efficient factory and production processes in the world, not least through automation in the Industrials sector. However, the shutdown of the Fukushima nuclear reactors, and the ensuing electricity shortages caused by the tsunami, forced many Japanese bosses to rethink domestic production lines and consider a shift overseas. In the 6 months that followed the tsunami, Japanese outbound M&A doubled in volume.

“Japanese management, weary of relentless decline in their home market and armed with a strong yen,are buying abroad.”

Additional factors causing Japanese investors to look overseas include:

- predictions that Japan’s population could shrink by 1/3 in the next 50 years offering little hope for domestic growth (source: Economist)

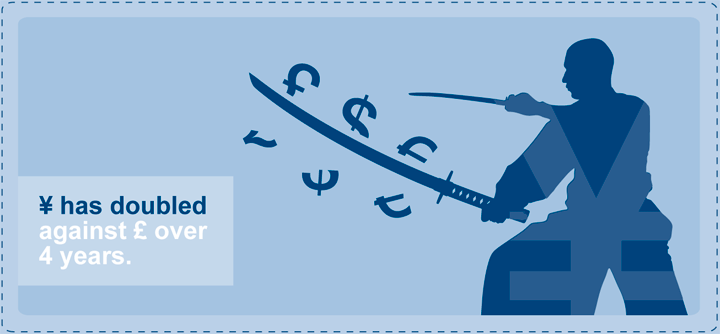

- the yen wreaking havoc on the competitiveness of Japanese exports, having doubled in value against the pound over the past 4 years

- neighbours (eg. South Korea) have kept their currency artificially weak in order to undercut Japanese exports

When Samsung of South Korea overtook Japan’s Panasonic in the global shipment of plasma televisions in February 2012 it was an uncomfortable reminder of how tough life has become for Japanese exporters.

The resulting upside is that the strong yen has handed Japanese companies a powerful acquisition weapon, roughly doubling their buying power for outbound transactions at a time of falling valuations in Europe. Four years ago it took 250 yen to buy one pound; now it costs just 120 yen.

Many Japanese companies are cash rich after years of austerity in the so called ‘lost decades’, in addition Japanese banks avoided the subprime crisis, enabling Japanese companies to borrow freely and relatively cheaply now. They have sizeable war chests to buy overseas – products, services, IP and even factories – at approximately half of the price. And they are taking advantage of it.

Thinking fast and slow

Japanese buyers can take time closing deals as they need to be wholly convinced of the strategic logic for an acquisition; they will commit time and resources to assessing the fit of a new business and the potential value it could create for the corporate ‘mother-ship’. Reaching consensus across multiple layers of the bidder company can extend the due diligence process (relative to typical Western timetables) but once a decision is reached by a Japanese buyer they will consider the financial implications quickly, make a bid and usually honour that price through to the close.

For product expertise Japanese acquirers will use their own employees’ in-depth evaluation and understanding of an asset, in addition to insights from management teams, before they commit to buying. They might include their R&D department long before they require any financial information.

Japanese buyers require different information at different points in their decision making processes and Western vendors need to be ready to adapt to this.

“Japanese buyers require different information at different points in their decision making processes.”

When advising on cross-border Japanese transactions involving Western companies, DC Advisory has learnt to throttle the flow of information depending on what buyers require to make a decision. We advise against ‘vanilla’ auction processes or rigid due diligence timetables. Many successful deals are ‘found in translation’ when misunderstandings and sequencing issues are avoided or resolved through clear communication, interaction and translation.

Talking heads

A diligent approach

The Japanese are renowned for the depth of their diligence, but buyers in the UK, continental Europe and Asia are also adopting a more diligent approach to transactions as they become more considered about the industrial logic behind a deal, often extending the transaction timetable.

The financial alchemy in the boom and the reliance on leverage to enhance returns has been replaced by a more strategic approach where the value must come from the industrial fit or the inherent strength of the target.

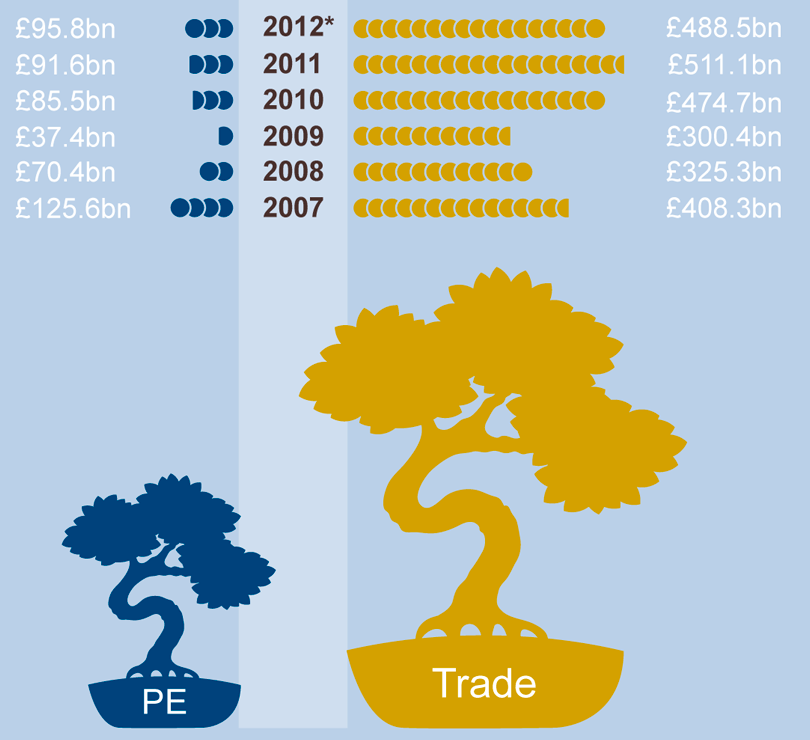

The landscape is calmer and bidders more cautious. However, in the mid-market there is little evidence of a retrenchment from either the private equity firms or trade buyers in terms of deal activity.

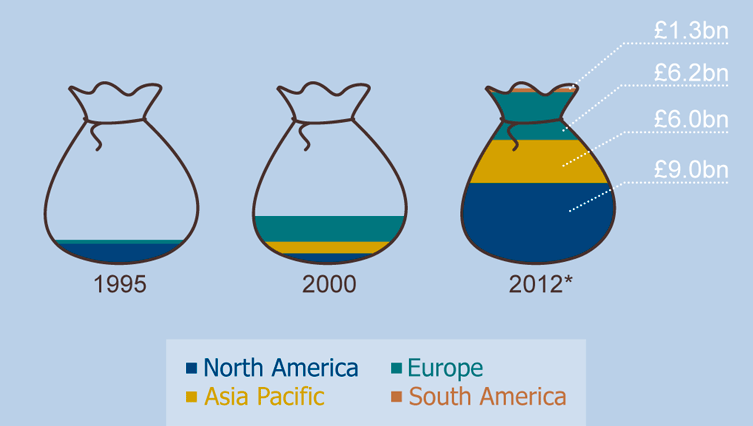

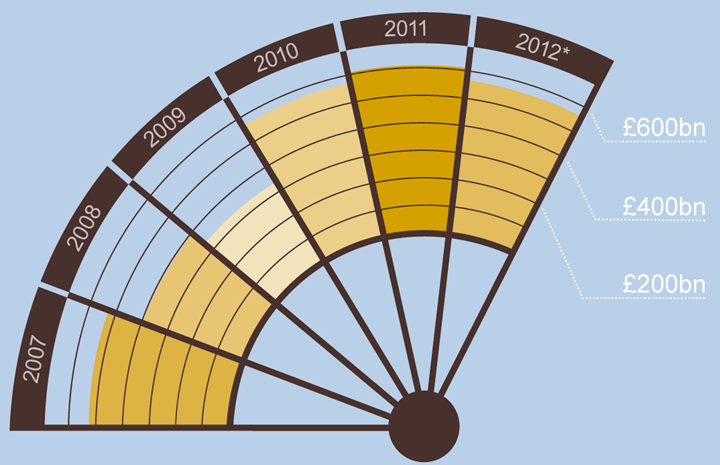

Value of mid-market M&A over time

The fact that deals are taking longer because of a Japanisation of the process is arguably a positive development.

“Deals are taking longer to close in our experience and vendors are being more selective”

Deals done for the right reasons without reliance on over-leverage are more likely to create long term value and this will help to restore global confidence in the M&A market amongst both participants and investors.

Many Japanese companies that have completed one successful outbound deal have gone on to do their second and third.

This virtuous cycle is growing in ever increasing circles in Japan where companies have shifted their approach to M&A significantly in the last 18 months. As a result, Japanese businesses are likely to continue buying overseas for as long as the yen remains strong and assets with tangible and intangible IP are for sale.

Global PE v Global Trade